IAN TAI [DECEMBER 18, 2019]

I was 18 when I was first introduced to the word: ‘Asset’.

A college mate handed me a copy of ‘Rich Dad Poor Dad’ and little did I know, it was to be the beginning of my journey as a student of accounting, finance, and investing without an end in sight. After a few sequels of Rich Dad’s books, I had made a switch from being a Science stream student to study accounting.

It was then I realised there is a difference between how accounting schools and Rich Dad define the word ‘Asset’ and knowing this is often a distinction of one’s financial destiny in the future. In other words, if you want to be financially rich, it behoves you to understand the definition of an asset so that you can invest in real assets and avoid an investment made to acquire fake assets.

Two Definitions of an Asset:

Here is how accounting schools define what an asset is:

An asset is a resource that a person owns or controls which has economic value.

Here is how Rich Dad define what an asset is:

An asset puts money into your pocket.

Accounting schools define an asset based on ownership or control. Meanwhile, Rich Dad’s definition of what an asset is is based on the direction of cash flow.

Personally, I use both definitions above in my finances. But, if you really wish to invest like the rich to attain financial freedom, I reckon the definition offered by Rich Dad over the other for Rich Dad’s definition of an asset enables us to make a distinction between a real investment asset from a fake one. For instance,

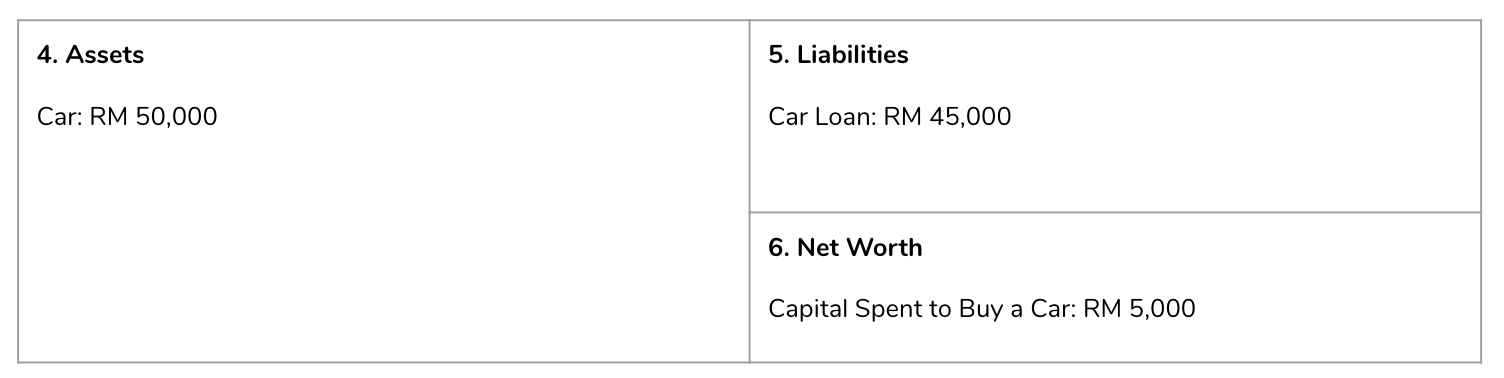

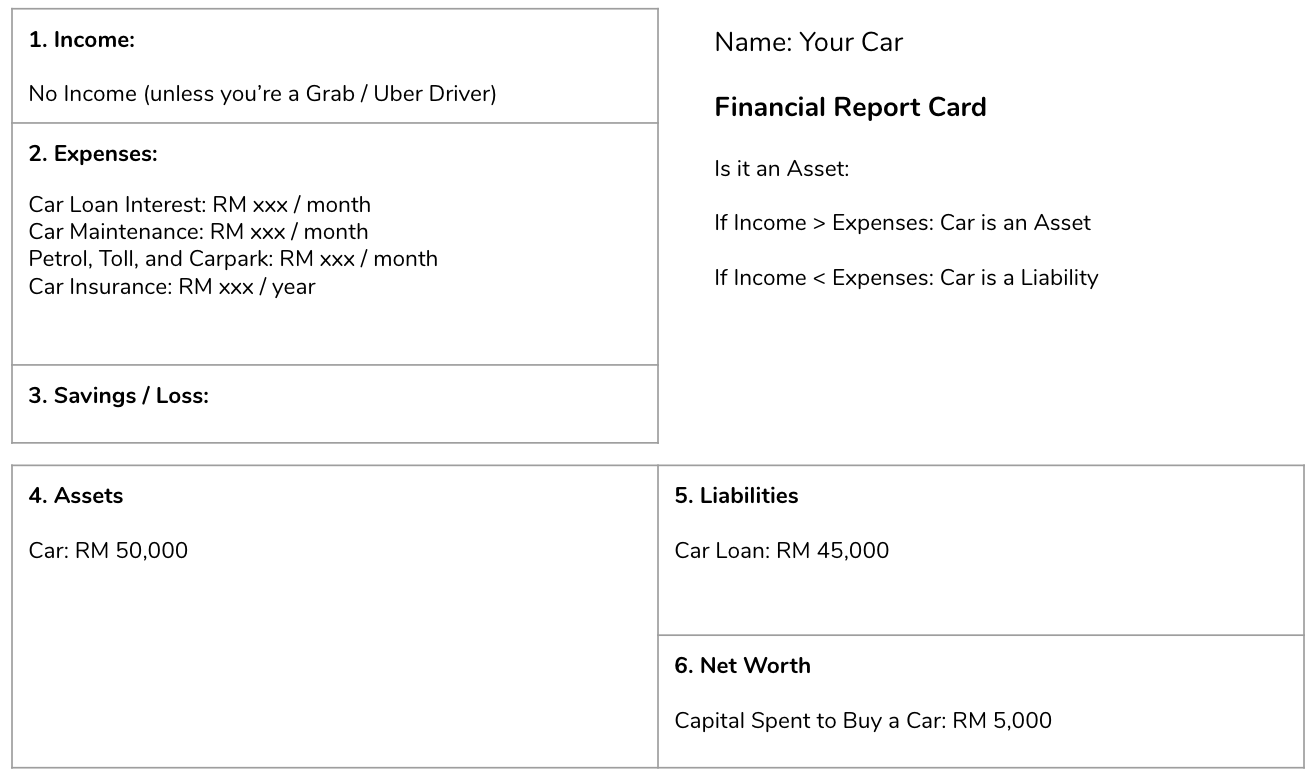

Is Your Car an Asset?

Based on the definition given by accounting schools, your car is an asset for it is an item which has economic value. Thus, if you purchase a Myvi for RM 50,000 where you place RM 5,000 in down payment and fund the remaining purchase with a RM 45,000 car loan, your financial statement would look like:

Meanwhile, under Rich Dad’s, your car is only classified to be an asset if it earns additional income which exceeds its expenses on a regular basis. Typically, your car would be deemed as a liability or a ‘Fake Asset’, unless you are able to make profits regularly from the usage of your car.

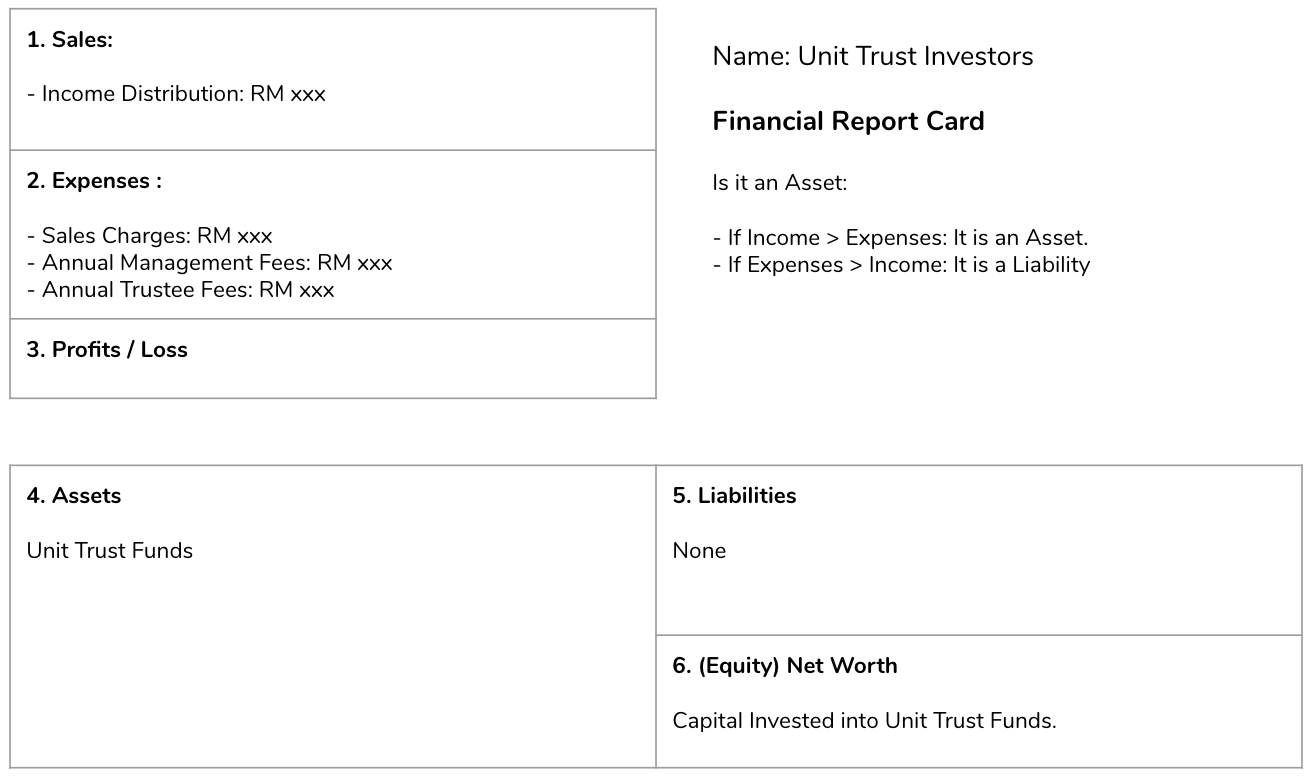

Are Unit Trust Funds ‘Real Assets’?

Once again, it depends on the direction of cash flow from your unit trust funds.

Are you receiving regular income distributions from your unit trust funds? Well, if your answer is ‘Yes’, then, the next question is: ‘Does your amount of income received to exceed your annual management and trustee fees?’ Thus, the bottom line is this: ‘If you are, from your unit trust investments:

– Earning more income distribution than annual fees paid, it is a Real Asset.

– Paying more Annual Fees than income received, it is a Fake Asset or Liability.

But, what about capital gains? What if my unit trust investments go up in prices in the future despite me paying more fees than income earned along the way?

Is it still a Fake Asset? a Liability?

Here is my sincere answer: Yes, it is still classified as a ‘fake asset’ until the time you sell it off for a profit, which is what most people hope to do in the future.

Let me give you an example.

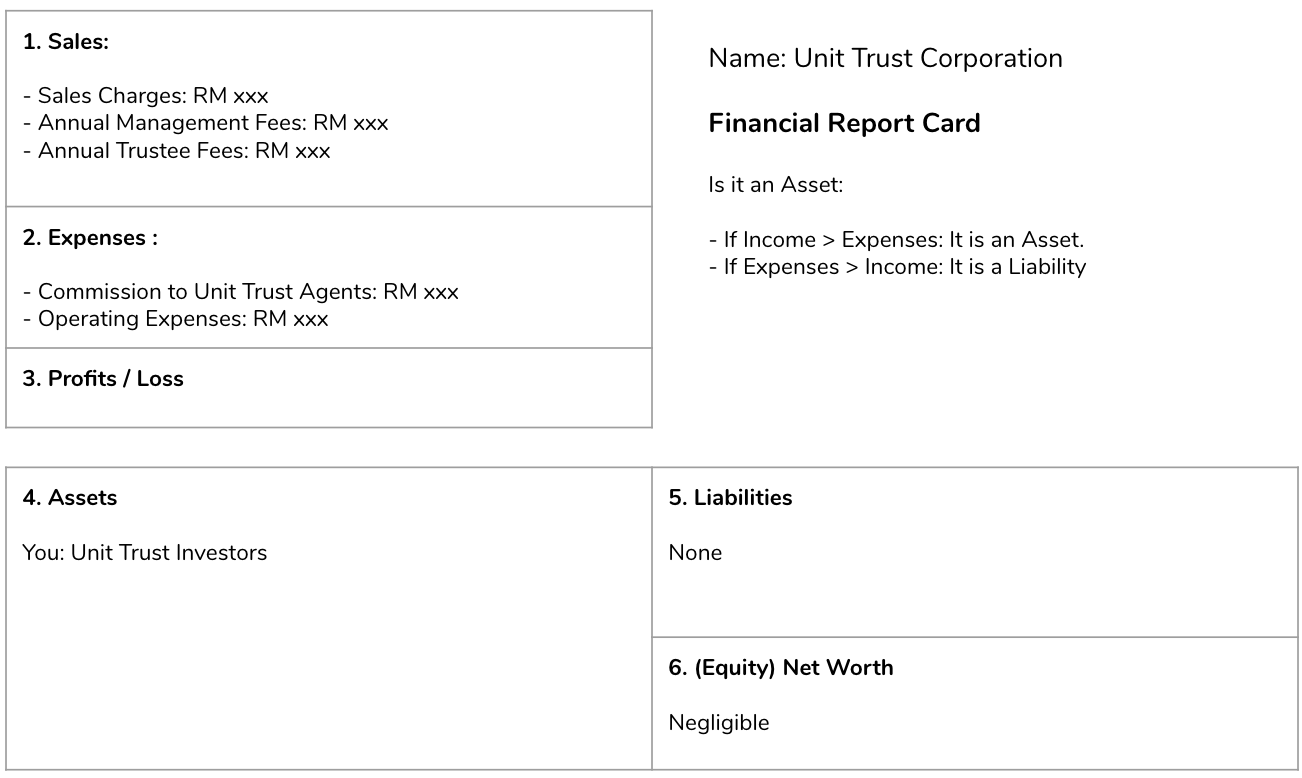

For instance, unit trust funds are often promoted as retirement schemes where people are suggested to ‘invest’ for the long-term, could be 10, 20, or 30+ years periodically, either monthly, quarterly, semi-annually or annually via the virtues of dollar-cost averaging into their preferred unit trust funds until the time when they decide to retire. In that 10, 20, or 30+ years, as you contribute to your unit trust funds, the financial statements for the unit trust funds would look like:

From the two statements above: Unit Trust Investors & Unit Trust Corporation, I believe we all can learn the difference between how ‘the rich’ invest differently from the others. They are as follows:

1. Cash Flows

Unit trust corporations are cash flow investors. They know what real assets are: Unit Trust Investors and they hope that their unit trust investors would remain faithful in contributing their capital into their funds for they would be receiving recurring income via fees for many years to come.

Unit trust corporations are cash flow investors. They know what real assets are: Unit Trust Investors and they hope that their unit trust investors would remain faithful in contributing their capital into their funds for they would be receiving recurring income via fees for many years to come.

2. Market Risk

Unit trust corporations are low-risk investors for their income are recurring and will flow into their bank accounts in all types of market conditions, good or bad in the future. In good market conditions, they collect higher fees as the value of your unit trust funds increase. In bad market conditions, they collect lower fees as the value of your unit trust funds decrease.

In a nutshell, unit trust investors invest 100% of the money into their preferred unit trust funds, takes 100% of the investment risks, and will only find out if the funds invested turned out to be a Real Asset or a Fake Asset in some 10, 20 or 30+ years (capital gain) down the road.

Meanwhile, unit trust corporations will be guaranteed a steady flow of income (cash flow) through annual fees for as long as you have capital in your unit trust funds. They are not obligated to compensate you if you lose money in a market downturn (risk protected).

Are Your Stocks ‘Real Assets’?

Let’s keep it local.

There are 900+ public listed companies listed on Bursa Malaysia.

How do you tell which of these stocks are ‘Real Assets’ and which are the ‘Fake’ ones?

Again, it all boils down to cash flow from your stock investments. Do you collect increasing dividends regularly from your stock portfolio? If you are, then, I’ll say that your stock portfolio consists of ‘Real Assets’ for they produce cash flow on a regular basis.

But again, what if I’m investing for capital gains?

Often, when people say that they are investing in ‘capital gains’, they could be saying the following:

1. They Intend to Earn Capital Gains by investing in Cash Flow Companies.

In essence, they are cash flow-oriented and would invest in stocks that produce both profits and cash flows consistently to its shareholders. Why? Stocks which have cash flow can choose to reinvest into expanding their businesses, making investments to buy up competitors, form joint ventures, acquire assets such as properties, hotels, plantation estates … etc to make additional earnings or cash flows in the future. Hence, the prices of these stocks would be revalued higher as they have increased their income by having more income-producing assets.

Stocks with rising cash flow (Real Assets) tend to bring long-term capital gains.

2. They are Stock Bettors, Gamblers, and Speculators.

Some may identify themselves as ‘stock traders who invest for growth’. This is a classic example of an identity crisis. They are confused as they do not know the differences between a stock investor and a stock trader. In most cases, they are just people who are trying their luck in stocks. How do I tell them apart from an investor or a stock trader? Simple. You just ask them for their game plan. If they buy stocks without a game plan, there you go: we have a stock speculator.

In short, how do I identify a stock that is a ‘Real Asset’ from many others which are ‘Fake Assets’? The answer lies in its Cash Flow, which is why value investors, including myself, study financial statements before investing in any stocks.

What about Your Properties?

Is your house an asset?

By now, you should have an idea on determining if your house is a Real Asset or a Fake Asset. If you are collecting monthly rental income, where it is more than all of your property-related expenses such as interest portion of your mortgage, maintenance fees, quit rent, assessment, repairs … etc, the property you own is a Real Asset. But, if you stay in your own house, it is a Fake Asset or a liability.

In a way, it is Cash Flow that determines the value of a property.

For instance, some opine that real estate is a good investment because it would double every 10 years once. Thus, these people would buy properties priced at, let’s say RM 500,000, hoping that they can be sold at RM 1 million after holding onto them for 10 years. Sounds like a plan, doesn’t it?

Well, let’s fast forward to the Year 2030 and you intend to sell off your property for RM 1 million, here’s a question: ‘Can you find buyers whose earnings are in the six-figures annually and have RM 200,000 in cash-in-hand to buy over your million-dollar property?’ Thus, if you could not find interested buyers who have the ‘cash flow’ to buy over your property, how then is it possible for you to be earning yourself capital gains from your property?

Conclusion: Cash Flow is the Name of the Game.

All in all, reading Rich Dad’s has shaped how I’m managing my finances and I’ve found it to be effective, especially in investing, be it stocks or real estate. This is influenced by the author’s emphasis on cash flow as a basis to determine if the investment is a ‘Real Asset’ or a ‘Fake Asset’.

So, do I become a better investor who invests in Real Assets and not Fake ones?

Ian Tai is the founder of DividenVault.com, a platform that empowers retail investors to build wealth through ownership of fundamentally solid stocks that pay ever-growing dividends year after year.

No comments:

Post a Comment